The Morning Hark - 19 Mar 2024

Today’s focus...BoJ deliver as expected but after 17 years was it worth the wait? RBA temper their enthusiasm for rate hikes

Overnight Highlights

Prices are at 6.45 GMT/2.45 EST, with changes reflecting movement from midnight GMT

Oil - Oil off a touch in Asia after yesterday’s further climb higher with Brent and Crude May futures trading at 86.70 and 82 respectively. The usual bid themes helping the sector; China growth, post data yesterday, Russian refinery drone strikes and Iraq also agreed to fall in line with the OPEC+ production cuts.

EQ - Asian equity markets mixed with the Hang Seng down one percent at 16,550. However the Nikkei up smalls post BoJ to 39,600 and little changed from yesterday’s open after the well telegraphed rate decision and dovish tone.

The US indices off smalls in Asia with the S&P and Nasdaq futures currently at 5208 and 18,185 respectively.

Gold - Gold off smalls in Asia with April futures currently trading at 2159 with the USD a touch firmer.

FI - Global yields softened a touch in Asia with the US2y and US10y futures yields currently at 4.73% and 4.32% respectively. The 10y broke back above 4.30% yesterday for the first time in 4 months as the market started to get nervous about the Fed dots. The curve is now pricing in less than three full cuts for this year, around 70bps.

European yields a touch firmer in line with the US with the German 10y at 2.46% and the Italian 10y yield at 3.68%.

UK gilt 10y similarly at 4.19%.

The JGB 10y currently off smalls to 0.74%.

FX - FX in Asia a little sparky post the central bank meetings. The USD Index currently at 103.78 and extending its gains on the back of yesterday’s higher yields. The majors; JPY, EUR and GBP currently at 150.45, 1.0865 and 1.2705 respectively. The JPY off close to one percent after the BoJ. Similarly the AUD weakening post RBA down over half of one percent to 0.6515.

Today’s FX option expiries today sees nothing of significance.

Others - Bitcoin and Ethereum off close to five percent and looking a tad vulnerable. Yesterday saw only the second day of ETF flows lead by the largest ever outflow form Grayscale’s GBTC. Currently the pair trading at 64,800 and 3355. Around 62k looks to be the real key level on the downside.

Macro Themes At Play

Recap

The final EU Inflation Report for February was bang on with headline and core YoY coming in as previously at 2.6% and 3.1% respectively.

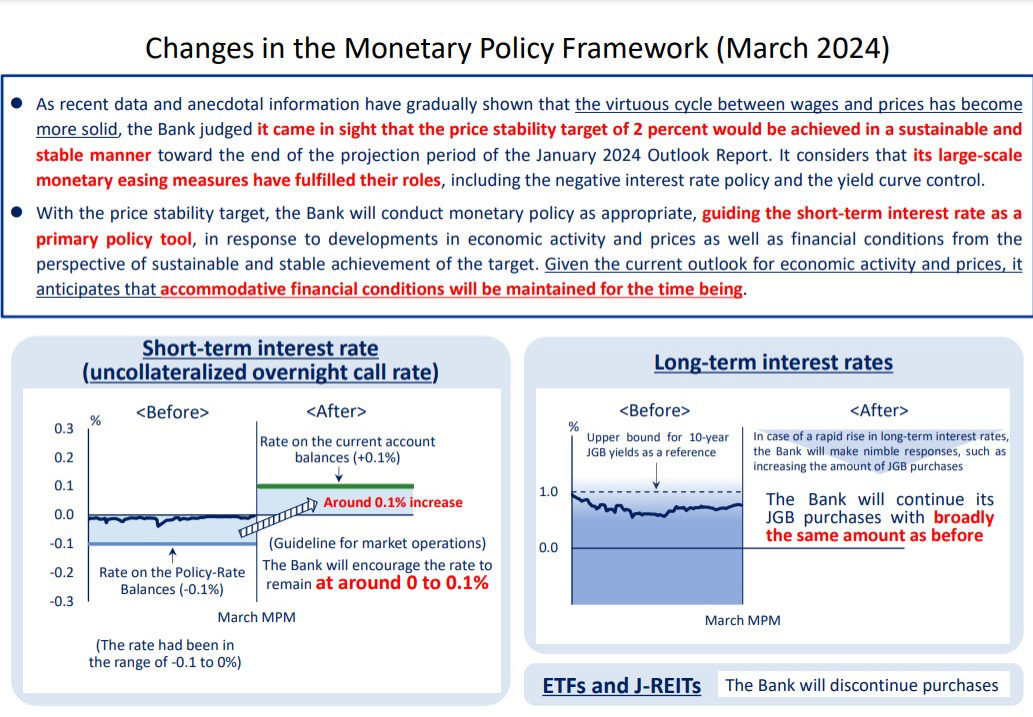

BoJ Review

Damp squib or what! Beautifully choreographed and telegraphed by the BoJ mouthpiece the Nikkei. As we said yesterday buy the rumour sell the fact. The main highlights:

The negative rates regime was ended with a 20bp hike taking rates to +0.1%;

YCC has gone with the removal of the target and reference rate;

However the Bank has committed to buying roughly the same amount of bonds and intervene with more if needed. Expectations are for the buying to be scaled back over time and proceeds will not be reinvested.

Risky asset purchases have been formally discontinued. Although the Bank had already pretty much ceased from purchasing ETFs and Real Estate Funds of late anyway; and

The massive stimulus package to stably achieve the 2% inflation target has been abandoned although the Bank stressed that monetary conditions would remain accommodative for the time being, ie they are not going to do a Fed/ECB and go on a hiking cycle.

Two dissenters in the ranks with Nakamura and Noguchi voting to keep negative rates.

Governor Ueda speaking as we go to press but sticking to basically the policy statement details:

We’ve confirmed a virtuous cycle of wages and prices;

Accommodative financial conditions will be maintained for the time being;

We will continue buying broadly the same amount of JGBs as before;

We will use the short term policy rate as our main tool;

Price target is now in sight; and

The pace of further rate hikes depend on the economy and price outlooks.

Source : BoJ

RBA Review

As expected they kept rates on hold at 4.35% but tempered somewhat their previous tightening bias. They included a new phrase in the statement which claimed the board are “not ruling anything in or out” but they have taken out “a further increase in interest rates cannot be ruled out”. They asserted that they had more confidence that inflation is returning to target.

Governor Bullock tried to put a touch of hawk in her press conference by insisting the board was not confident enough to say they can rule out more rate hikes. Furthermore the inflation war is not yet won and risks remain on both sides of policy.

Market wise the initial reaction is the AUD has sold off smalls as have yields. The market is now pricing in roughly 43bps of cuts this year up from the mid 30s previously.

The Aussie banks a touch split in what they expect from the RBA with CBA the outlier with 3 cuts this year, starting in September. Westpac sees 2 with the first in September whilst NAB and ANZ see one only in q4.

Central Bank Speakers

ECB’s de Guindos stressed that the evolution of wages was key and the ECB will have more information in June. Again the ECB is data dependent not Fed dependent.

The Day Ahead

All faded into the background amidst the BoJ announcement but we had some poor data out of Japan with Capacity Utilisation falling 7.9% in January its biggest fall in over 18 months. In addition the final January print for Industrial Production came in at -6.7% the worst since the middle of the pandemic.

ZEWs main focus for the morning as well as some outdated Eurozone Wage Data for q4. The afternoon takes us to the February Canadian Inflation Report as well as some US Housing Data.

Overnight its all about the Chinese Loan Prime Rate announcements and just before we go to print we have the February UK Inflation Report.

👏 If you found this briefing helpful, please show the desk some appreciation by giving it a ‘Like’ or a ‘Comment’ at the bottom of the page.

Stay on top of the latest market narratives throughout the day using our curated research & commentary channels on Harkster.com

Main Highlights Ahead

All times in GMT (EST+4 / CET-1 / JST-9)

The main highlights for the day ahead ahead in terms of data and speakers:

Tuesday

EU ZEW Economic Sentiment Index Mar consensus vs previous 25 (10.00 GMT)

EU Labour Cost Index YoY q4 consensus % vs previous 5.3% (10.00 GMT)

EU Wage Growth YoY q4 consensus % vs previous 5.3% (10.00 GMT)

Germany ZEW Economic Sentiment Index Mar consensus 20.5 vs previous 19.9 (10.00 GMT)

Canada Inflation Rate MoM Feb consensus 0.6% vs previous 0% (12.30 GMT)

Canada Inflation Rate YoY Feb consensus 3.1% vs previous 2.9% (12.30 GMT)

Canada Core Inflation Rate MoM Feb consensus % vs previous 0.1% (12.30 GMT)

Canada Core Inflation Rate YoY Feb consensus % vs previous 2.4% (12.30 GMT)

US Building Permits Feb Prel consensus 1.495m vs previous 1.489m (12.30 GMT)

US Housing Starts Feb consensus 1.425m vs previous1.331m (12.30 GMT)

ECB Speakers

de Guindos (08.30 GMT)

Early Wednesday

China Loan Prime Rate 1y consensus for rates to remain on hold at 3.45% (01.15 GMT)

China Loan Prime Rate 5y consensus for rates to remain on hold at 3.95% (01.15 GMT)

UK Inflation Rate MoM Feb consensus 0.7% vs previous -0.6% (07.00 GMT)

UK Inflation Rate YoY Feb consensus 3.5% vs previous 4% (07.00 GMT)

UK Core Inflation Rate MoM Feb consensus 0.7% vs previous -0.9% (07.00 GMT)

UK Core Inflation Rate YoY Feb consensus 4.6% vs previous 5.1% (07.00 GMT)

Good luck.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.